GLENDOWER: I can call spirits from the vasty deep.

HOTSPUR: Why, so can I, or so can any man - but will they come…?

Such has been the dilemma faced by the central banking community, increasingly so: policy officials have the same apparent ability as Shakespeare’s Glendower (based on one Owain Glyndŵr, the last native Welshman to hold the title of “Prince of Wales”), yet the characteristic response from markets has been just as capricious as Hotspur’s retort suggests: just because you say it's easing doesn't necessarily make it so...

Fiat policy is successful not by

virtue of the exhortation, but by manifestation of that which has been

prescribed. It’s one thing to say you’re easing, quite another to convince

markets of it.

|

| Owen Glyndŵr of Wales, Fiat Policy Pioneer |

The difference, perhaps, is that while the character

in Henry IV seems to have genuinely “believ’d the magic wonders which he sang”,

central bankers should be more acutely aware of the wide gulf between saying

& doing. Indeed, the pragmatic response has been to join edict with act to

the point that we now have policy prescription written in no uncertain terms

(“yield curve control”).

On the threshold now of the first rate cut by the

Federal Reserve since 2008, this question has to be even more vexing for those

about to do the cutting. At this point, is a 25bp cut alone enough to “ease”?

The simple answer is no.

“What’s priced in” for Wednesday is not just

equivalent to EFFR – yield(FFQ9). That’s because, however small the likelihood

of an “on-hold” result, there is closer to a trinomial decision tree that must

be followed for each meeting.

As a result, the entire curve & options

surface needs to be fit to a weighted probability across each possible path

that policy could follow this year – resulting in a solution that yields a

small but not insignificant possibility of “on-hold”.

Over the past 2 weeks,

the rank order of 10 most likely paths for policy this year as determined by

the shape of the options surface + Fed Funds curve have stayed mostly constant,

with the exception of Williams’ outburst on the 18th (which left

more than 50% odds priced for just one of two outcomes: 1) July -50 followed by

another -25 later in the year, and 2) July -25 followed by -50 in September).

Every path to which the options + Fed Funds markets

have assigned a greater than 1% probability at some point in the last 2 weeks

are shown below.

Across all possible outcomes, we can sum up the

“on-hold” vs -25 vs -50 July policy actions to give a better idea of what

front-end assets are priced for.

Like Hotspur, Fed officials may be wondering how a

delivered 25bp cut in July alone will actually “ease”.

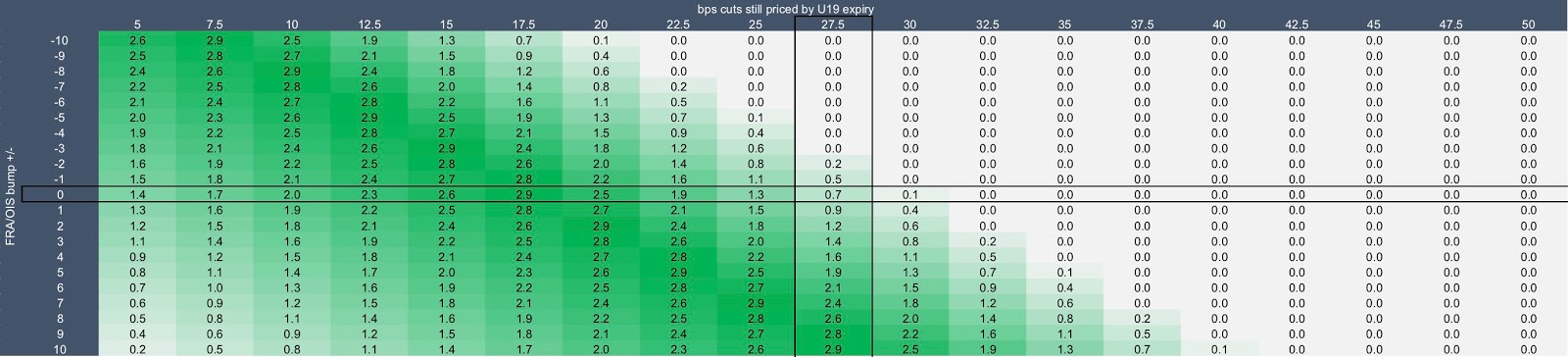

TRADE: EDU9 1x1.5 PUT SPREADS

For choice, I like the following here as a low premium way to position for the Fed to disappoint dovish expectations in the front end: Buy EDU9 97.875/97.75 1x1.5 ps for 4.25

Trade pays out 3x if we reduce the number of 25bp cuts by just half a cut 2 days before the September FOMC. Since it expires before the Sep FOMC, there should at least something priced for each of the Sep & Oct meetings (+ a few days’ worth of Dec).

Net PNL shown below under various shocks to FRA/OIS (+/- Xbps) and the bps worth of cuts still priced into U19->3mth OIS.

Payout Ratios below (i.e. gross PNL / premium):

Additional discussion & consideration below...

A BLUNT MONSTER WITH UNCOUNTED HEADS:

Let’s not kid ourselves either, to say the current Fed

roster has had a mixed track record of successful communication with markets

would be charitable. For the 8 meetings over the past year, 4 of those took

place ostensibly while the Fed was still in “tightening” mode: however, all 4

saw 5yr Treasury yields rally by more than a 1-day standard deviation within 24

hours.

After the Fed’s January 2019 “pivot”, the price action

has been more consistent with an increasingly dovish bias – unless you count

the May FOMC, of course.

But, to put a finer point on the issue facing the Fed

this week, controlling front-end yields by mechanically moving the overnight

rate is only one part of the equation. Sceptics might refer to Wednesday’s

decision as “data-independent easing”, but even Janet Yellen opined this

weekend on the global dynamics which have conspired to drive the Fed back

towards a cut in rates less than 9 months after the last hike. So, the effect that the Fed’s action will have on currency markets (and equities, for that matter), is perhaps even more important.

UNEASY LIES THE HEAD:

The Fed is not ignorant of this fact, of course. Policy officials are well-aware that, for example, the average daily annualized return on a long position on the S&P has been 6.8% over the last 25 years – of which a little over 1/3 is earned on average on the 8 days a year that the FOMC renders its verdict on policy. By the same token, going short the USD versus a basket of G10 FX has had an average daily annualized return of around 30bp over that same time period, but doing that only on FOMC dates would do about 2.5 times better. That’s despite the fact the Fed has raised front end rates on 36 days over that time period, versus cutting them on 29.

It would seem as though this is a point in favour of Glendower being able to summon spirits to his aide. However, a crucial detail is omitted – the critical element of surprise.

This dovish skew is because of a risk-avoidance policy by central banks who would rather err on the side of a dovish surprise. For every June 2013 or March 2014 where the market reacted hawkishly, there’s a September 2013, March 2015, or March 2016 where the market saw a much more substantial dovish reaction. Indeed, we’ve seen our fair share of “dovish hikes” (June 2004, June 2006, March 2017, etc), but the contrasting example has been far more infrequent – though not entirely sui generis. Markets evolve, of course, and have begun to anticipate such skew to the distribution, e.g. “Pre-FOMC Drift”. If central bankers know that market participants believe they are being rewarded by staying invested in an asset other than cash, then there has to be some additional incentive to stay allocated thusly when policy “eases”: enter the value of surprise.

UNEASY LIES THE HEAD:

The Fed is not ignorant of this fact, of course. Policy officials are well-aware that, for example, the average daily annualized return on a long position on the S&P has been 6.8% over the last 25 years – of which a little over 1/3 is earned on average on the 8 days a year that the FOMC renders its verdict on policy. By the same token, going short the USD versus a basket of G10 FX has had an average daily annualized return of around 30bp over that same time period, but doing that only on FOMC dates would do about 2.5 times better. That’s despite the fact the Fed has raised front end rates on 36 days over that time period, versus cutting them on 29.

|

| Sir Henry Percy, for whom the other London club is named. |

It would seem as though this is a point in favour of Glendower being able to summon spirits to his aide. However, a crucial detail is omitted – the critical element of surprise.

This dovish skew is because of a risk-avoidance policy by central banks who would rather err on the side of a dovish surprise. For every June 2013 or March 2014 where the market reacted hawkishly, there’s a September 2013, March 2015, or March 2016 where the market saw a much more substantial dovish reaction. Indeed, we’ve seen our fair share of “dovish hikes” (June 2004, June 2006, March 2017, etc), but the contrasting example has been far more infrequent – though not entirely sui generis. Markets evolve, of course, and have begun to anticipate such skew to the distribution, e.g. “Pre-FOMC Drift”. If central bankers know that market participants believe they are being rewarded by staying invested in an asset other than cash, then there has to be some additional incentive to stay allocated thusly when policy “eases”: enter the value of surprise.

THE BETTER PART OF VOL, IS DISCRETION:

The same is true for volatility. Enterprising academics

(displaying an intrepid approach to risk-management that might make even the

most generous CRO blanch, might I add) have noted that excess returns on short

straddle positions taken the day before the FOMC & covered the day after.

For example, the left-most column suggests “Mean” 9.3% historical returns from

short straddle positions on the first ED contract.

|

| Link: https://www.frbsf.org/economic-research/files/wp2019-12.pdf |

Indeed, while it’s fashionable to bemoan the general

lack of implied volatility in markets today, the fact is that violent shocks

have more frequently pierced an otherwise quiescent surface. If we define a

significant shock as a 1-day return which is more than 5 standard deviations

away from the daily average return of the preceding 33, the S&P has seen 4

such days in the last 3 years. That compares to 14 such days in the prior 45

years. Indeed, to find the last time you’d have seen 4 days that generate

returns as outsized relative to the preceding month, you’d need to go back to

the last time geopolitics convulsed to such an extent that the World was

considered to be at War.

Nor is this unique to equity markets: the number of

so-defined “5-sigma events” over a 3-year rolling block has been increasing

across asset classes over the post-crisis period.

|

| Source: Neuron Advisors, Robert Hillman, Bloomberg |

ECB - A CASE STUDY:

On that note, it’s worth contemplating the move that

European assets saw last week when the ECB stayed the course by setting the

stage for a cut in the fall (disappointing those who were hoping for a more

immediate policy prescription).

| ||

Equity markets & FX reacted in kind, taking their

lead initially from the move in rates as the best kind of curve move for bank

equities appeared in the offing, before collapsing back to the day’s opening

levels as the worst kind of curve move for bank equities was realized instead.

It’s well-known that Draghi is particularly sensitive

to intra-day moves preceding his press conference & last Thursday’s move

appears to have been just that: markets became overly optimistic about the

likelihood for an overtly dovish message from the ECB President after foregoing

a cut & Draghi didn’t take the bait.

Keep in mind that Draghi is literally the most

seasoned central bank president at the helm of a developed currency as a known

quantity to market participants (Thomas Jordan at the SNB is a close second; I

don’t count Carney’s dual stint between BOC & BOE, and because he’s hardly

a model for tamping down on unrealistic market expectations).

No matter how it’s

positioned in the press conference on Wednesday, Powell will be faced with the

prospect of recalibrating market expectations which were – at a minimum on an

absolute basis – off by about 4bps on the overnight rate as the wings of the

distribution are clipped. As the market digests the participants’ expectations

for policy forthcoming & an immediate end to QT before the press

conference, note that the “most likely” path that the market assigns today to

2019 policy action is consecutive cuts of 25bps at each remaining meeting. The

next 6 “most likely” paths (not counting the 1 path where no action is taken at

all) represent fewer cumulative cuts (and with no policy action at not one but

two meetings remaining this year). Table from earlier shown again for emphasis:

Glendower, himself, might shy away from such a task.

A few takeaways:

1. It’s a very high hurdle indeed for the Fed to pull

off a dovish ease at Wednesday’s meeting.

2. Don’t expect the press conference to unveil some

previously unforeseen boon to the dove’s cause.

3. Position for what the Fed will do, not what they

should.

4. To the extent a cut is positioned as a one-off to

pre-emptively cushion the economy against a shock, we’re back to trading SPX

digitals.

5. Better to play the odds as they are reallocated

across the options surface following Wednesday’s meeting.